Buy Now Pay Later is transforming the way people shop online by making purchases more flexible and accessible. Instead of paying the full price at once, shoppers can divide their payments into easy installments without extra hassle. This simple concept has made online shopping more convenient, helping consumers manage their budgets better while still enjoying the products they want right away.

In today’s fast-growing digital world, Buy Now Pay Later (BNPL) is reshaping consumer credit and business models alike. It encourages responsible spending while boosting sales for online retailers. By bridging the gap between affordability and instant gratification, BNPL has become one of the most innovative financial trends of modern e-commerce.

What Is Buy Now Pay Later (BNPL)?

Buy Now Pay Later (BNPL) is a modern payment solution that allows consumers to purchase goods or services immediately and pay for them later in smaller, interest-free installments. Instead of paying the full amount upfront, shoppers can divide the total cost into equal payments spread over weeks or months. This concept has gained massive popularity in online shopping because it offers both convenience and flexibility, especially for those who prefer to manage their cash flow efficiently.

The Buy Now Pay Later (BNPL) model works in a simple way. When a customer checks out on an e-commerce site, they can choose the BNPL option instead of paying in full. The BNPL provider then pays the merchant right away, and the customer repays the provider over time. This arrangement benefits both sides: consumers get instant access to products, and retailers receive guaranteed payments without delay.

Several leading platforms have made Buy Now Pay Later (BNPL) services mainstream. Popular providers include Klarna, Afterpay, PayPal Pay in 4, Affirm, and Zip. These platforms partner with major online retailers and integrate directly into checkout pages, making the payment process quick and seamless. With mobile apps and digital wallets, customers can also track their upcoming payments and spending history easily.

Unlike traditional credit cards or loans, Buy Now Pay Later (BNPL) doesn’t always require a credit check or charge high interest. It focuses on affordability and accessibility, particularly for younger shoppers who want to avoid long-term debt. BNPL offers a new kind of financial freedom, reshaping how people think about shopping, spending, and short-term credit in the digital age.

How Buy Now Pay Later (BNPL) Is Changing Online Shopping?

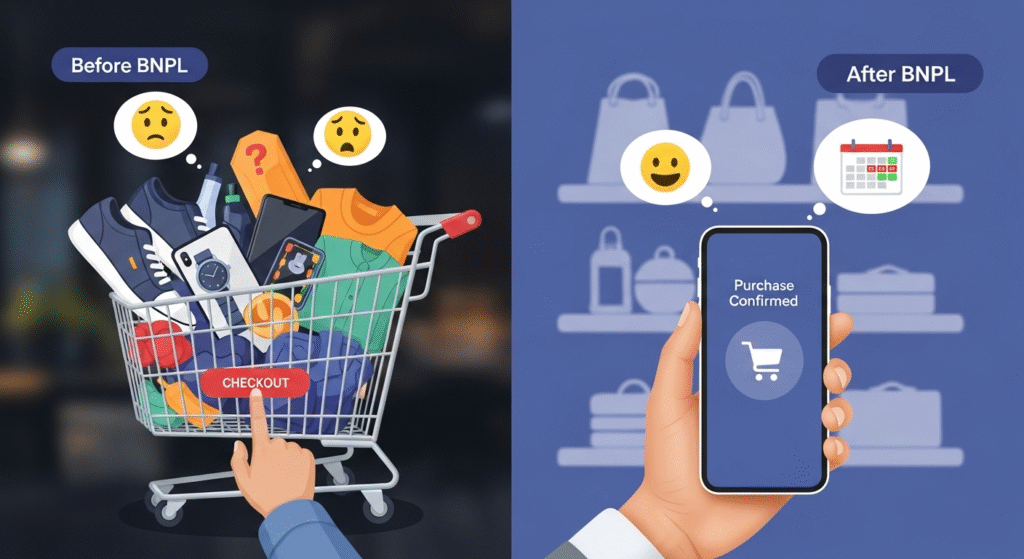

The rise of Buy Now Pay Later (BNPL) has completely changed the way people shop online. It gives consumers more control over their purchases by allowing them to pay in flexible installments rather than all at once. This system helps shoppers manage their budgets while still enjoying immediate access to the products they want. For many, BNPL removes the financial barrier that often prevents large purchases, boosting overall confidence in online shopping.

By offering Buy Now Pay Later (BNPL) at checkout, retailers have noticed significant growth in conversion rates and sales. When customers realize they can pay later without interest, they are more likely to complete the purchase instead of abandoning their carts. This directly improves sales performance and customer satisfaction. Moreover, BNPL promotes a smoother checkout process, creating a faster and more enjoyable shopping experience. The ease of splitting payments encourages repeat purchases, fostering long-term customer loyalty.

Buy Now Pay Later (BNPL) also influences consumer behavior. Shoppers feel more comfortable buying higher-priced items because the financial burden is spread over time. However, this convenience can sometimes lead to impulse buying, as customers perceive payments to be smaller and more manageable. Retailers leverage this behavior through targeted promotions, offering BNPL options during peak sales or limited-time offers to increase transaction volume.

Impact on Consumer Credit

Buy Now Pay Later (BNPL) is redefining how people use and understand consumer credit. It provides easy access to short-term financing without the complexity of traditional loans or credit cards. Shoppers can make purchases instantly and pay later in scheduled installments, helping them better manage cash flow and short-term expenses. For individuals with limited credit history, BNPL can be a practical entry point to experience responsible borrowing in a digital-first environment.

One of the most notable advantages of Buy Now Pay Later (BNPL) is accessibility. Many BNPL providers do not require a full credit check, making it easier for consumers to get approved. This inclusivity allows users from various financial backgrounds to shop confidently online. However, as BNPL usage grows, its influence on consumer credit becomes more significant. Some providers now report payment activity to credit bureaus, which can help responsible users build or improve their credit scores over time.

Despite these benefits, Buy Now Pay Later (BNPL) comes with potential risks. The convenience of splitting payments can lead to overspending if consumers lose track of multiple active installments. Missing payments or defaulting may result in penalties, interest charges, or even negative credit reporting. Therefore, financial literacy plays an essential role in responsible BNPL usage. Consumers should fully understand repayment schedules, due dates, and the impact of delayed payments on their financial health.

Benefits for Businesses

Buy Now Pay Later (BNPL) is not just a tool for consumers, it’s also a powerful advantage for online businesses. By offering flexible payment options, companies can attract more customers and improve overall sales performance. BNPL makes high-value items more accessible to a larger audience, removing financial hesitation at checkout. When shoppers can pay later in easy installments, they feel more confident making purchases, which directly boosts conversion rates for retailers.

One of the biggest benefits of Buy Now Pay Later (BNPL) for businesses is enhanced customer retention and loyalty. When customers enjoy a seamless payment experience, they are more likely to return for future purchases. BNPL encourages repeat buying behavior because it builds trust and convenience into the shopping process. Businesses that integrate BNPL at checkout also tend to see a reduction in cart abandonment rates, since shoppers are less worried about immediate costs.

Another major advantage of Buy Now Pay Later (BNPL) is the increase in average order value (AOV). Customers are more willing to buy additional items or upgrade to premium products when payments are divided over time. This directly increases revenue per transaction. Furthermore, BNPL helps businesses reach new demographics, especially younger consumers who prefer digital-first and interest-free payment methods over credit cards.

Challenges and Regulatory Concerns

While Buy Now Pay Later (BNPL) offers great convenience, it also faces several challenges and growing regulatory attention. One of the key concerns is the lack of consistent financial regulation in many regions. Because BNPL is still relatively new, it often operates outside traditional lending rules. This can lead to inconsistent practices between providers and confusion for consumers who might not fully understand the repayment structure or potential penalties.

Data privacy is another major concern in the Buy Now Pay Later (BNPL) space. As customers provide personal and financial details to multiple BNPL platforms, there is a growing risk of data misuse or security breaches. Companies must ensure strong data protection measures to maintain customer trust. Consumer protection authorities are also calling for greater transparency, ensuring users are clearly informed about repayment schedules, late fees, and the impact of missed payments on their credit.

Another challenge of Buy Now Pay Later (BNPL) is the risk of overspending. Because payments feel smaller and more manageable, users may buy more than they can afford. This raises concerns about debt accumulation and financial stress, especially among younger consumers. Regulators are increasingly focusing on creating responsible lending standards to prevent misuse and ensure financial stability.

The Future of BNPL and Digital Finance

The future of Buy Now Pay Later (BNPL) looks promising as it continues to evolve with modern financial technology. With the rise of AI, blockchain, and digital wallets, BNPL is becoming smarter, faster, and more secure. Artificial intelligence helps personalize installment plans based on a user’s spending behavior, while blockchain ensures greater transparency and trust in transactions. As these technologies mature, BNPL will likely become a key pillar in the digital finance ecosystem.

Global market trends show that Buy Now Pay Later (BNPL) usage will continue to grow rapidly. E-commerce expansion, mobile payments, and the increasing preference for interest-free credit options are driving adoption. Financial institutions and retailers are also collaborating more closely to integrate BNPL solutions across various industries — from fashion and travel to healthcare and education. This diversification shows how BNPL is expanding beyond shopping into broader areas of consumer finance.

Another exciting development for Buy Now Pay Later (BNPL) is its potential to enhance financial inclusion. Many people without access to traditional credit systems can now enjoy flexible, manageable payment options. As regulators introduce new standards, BNPL will become more transparent and secure, increasing consumer confidence globally. Integration with digital banking and fintech innovations will make these systems even more efficient and reliable.

Conclusion

Buy Now Pay Later (BNPL) has completely changed the way people shop and manage money online. It gives consumers the freedom to purchase what they need instantly while paying later in small, manageable installments. For businesses, it boosts sales, increases loyalty, and builds trust with digital shoppers. However, responsible use and proper regulation are essential to prevent overspending and ensure financial stability. As technology continues to advance, Buy Now Pay Later (BNPL) will remain a key part of modern finance—combining convenience, flexibility, and innovation. It’s more than just a payment option; it’s a smarter way to connect consumers and businesses in the digital economy.

FAQs

Is Buy Now Pay Later (BNPL) safe to use for online shopping?

Yes, Buy Now Pay Later (BNPL) is generally safe when used through trusted platforms like Klarna, Afterpay, or PayPal. These services use strong security measures to protect your data and payments. However, it’s important to read the terms carefully before using them. Always make payments on time to avoid penalties or hidden charges. When used responsibly, BNPL can be a secure and helpful way to manage short-term spending.

Can using Buy Now Pay Later (BNPL) affect my credit score?

Buy Now Pay Later (BNPL) may affect your credit score depending on the provider. Some companies report your repayment activity to credit bureaus, while others don’t. If payments are made on time, BNPL can help build your credit history. However, missing payments or defaulting may harm your score. Always check your provider’s policy before using the service, and ensure you manage payments carefully to maintain a healthy financial record.

Who can apply for Buy Now Pay Later (BNPL) services?

Anyone with a valid ID, bank account, and steady income can apply for Buy Now Pay Later (BNPL). Most platforms perform a soft credit check or basic verification to confirm your ability to repay. Young adults and online shoppers often use BNPL because it offers fast approval without complex paperwork. The eligibility criteria may vary by country or provider, but overall, BNPL is designed to be accessible and user-friendly for most consumers.

What happens if I miss a Buy Now Pay Later (BNPL) payment?

If you miss a payment with Buy Now Pay Later (BNPL), you might face late fees or temporary suspension of your account. Some providers also report missed payments to credit bureaus, which can lower your credit score. It’s important to track payment schedules and set reminders to avoid penalties. Most BNPL apps send notifications before the due date, so staying alert and paying on time keeps your account in good standing.