Life insurance planning helps you protect your family’s financial future and gives peace of mind. It ensures your loved ones are financially safe if something unexpected happens. With the right plan, you can cover daily expenses, debts, and long-term goals like education or home security.

Life insurance planning in this guide explains simple strategies to choose the right coverage for your needs. You will learn how to match policies with your income, responsibilities, and future plans. In this guide, you will also understand why early planning is important for long-term financial stability.

Types of Life Insurance Policies

Life insurance planning starts with understanding the different types of life insurance policies available. Each policy is designed to meet specific financial needs and family goals. The most common type is term life insurance, which provides coverage for a fixed period, such as 10, 20, or 30 years. It is affordable and ideal for families who want simple protection during key earning years. Life insurance planning with term policies works well for covering loans, education costs, and daily expenses.

Another option is whole life insurance, which offers lifelong coverage along with a savings component. This policy builds cash value over time and can be useful for long-term financial security. In life insurance planning, whole life policies are often chosen by people who want stable premiums and guaranteed benefits. Universal life insurance is more flexible, allowing changes in premiums and coverage amounts as financial situations change.

There is also endowment and investment-linked insurance, which combines protection with savings or investment features. These policies can help in long-term goals such as retirement or children’s education. Life insurance planning becomes easier when you understand how each policy balances risk protection and savings.

Choosing the right policy depends on income, age, family size, and future responsibilities. Life insurance planning is not about picking the most expensive policy but selecting the one that fits your financial situation. By knowing the types of life insurance policies, you can make informed decisions and build a strong foundation for your family’s financial future.

Assessing Your Family’s Financial Needs

Life insurance planning requires a clear understanding of your family’s financial needs. This step helps you identify how much support your loved ones would need if you are no longer there. Start by listing daily household expenses such as food, utilities, rent, and transportation. Life insurance planning should also consider long-term needs like children’s education and healthcare costs.

Next, calculate all existing debts, including home loans, personal loans, and credit cards. These obligations should not become a burden on your family. In life insurance planning, covering debts is a top priority to maintain financial stability. You should also think about future goals, such as weddings, higher education, or retirement support for your spouse.

Income replacement is another key factor. Ask yourself how many years your family would need financial support. Life insurance planning often suggests replacing income for at least 10 to 15 years. This ensures your family can maintain their standard of living.

Savings and existing assets should also be reviewed. If you already have savings, investments, or employer-provided insurance, these can reduce the required coverage amount. Life insurance planning is most effective when it balances protection with available resources.

Choosing the Right Coverage Amount

Life insurance planning is incomplete without choosing the right coverage amount. The coverage should be enough to support your family’s lifestyle, pay off debts, and meet future goals. A common approach in life insurance planning is to calculate coverage as a multiple of your annual income, usually 10 to 15 times. This provides a basic guideline for protection.

Start by adding all financial responsibilities, including loans, education costs, and daily expenses. Then subtract existing savings and investments. Life insurance planning focuses on filling the gap between what your family needs and what they already have. This method ensures accurate coverage without overpaying for premiums.

Your age and health also influence coverage decisions. Younger individuals can secure higher coverage at lower premiums, making early life insurance planning more affordable. Inflation should also be considered, as future expenses will likely increase over time.

Avoid choosing coverage based only on affordability. While budget matters, life insurance planning prioritizes adequate protection. Underinsuring can leave your family financially vulnerable. Reviewing coverage regularly is also important, especially after major life events like marriage or having children.

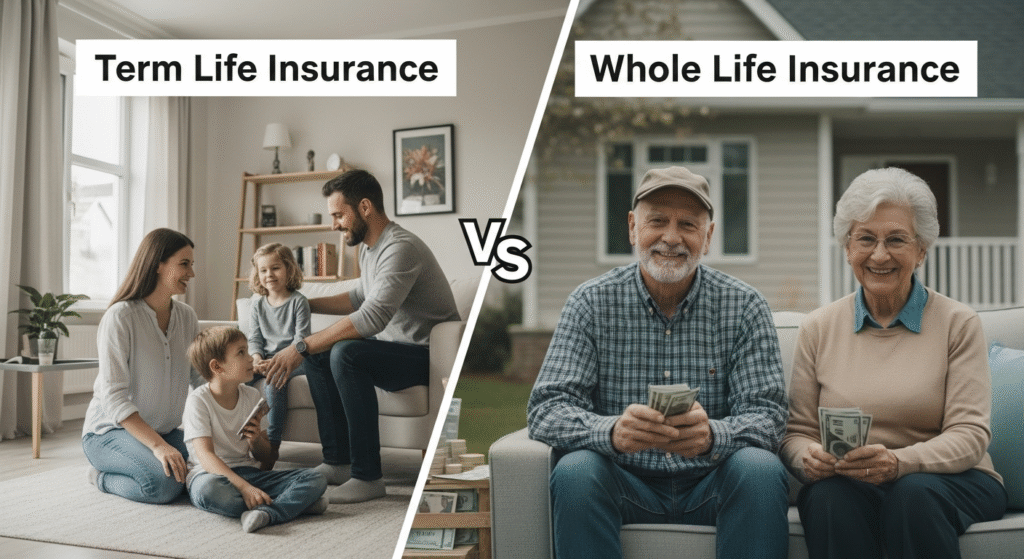

Term vs Whole Life Insurance

Life insurance planning often begins with comparing term life insurance and whole life insurance. Both options provide financial protection, but they work in different ways. Term life insurance offers coverage for a fixed period, such as 10, 20, or 30 years. It is simple and affordable, making it popular in life insurance planning for young families. This policy pays a benefit only if the insured person passes away during the term. It is ideal for covering temporary needs like loans, education costs, and income replacement.

Whole life insurance, on the other hand, provides lifetime coverage. In life insurance planning, whole life insurance is often chosen for long-term security. It includes a savings feature called cash value, which grows over time. This cash value can be borrowed or used later in life. Premiums are usually higher, but they remain fixed. Life insurance planning with whole life insurance suits people who want guaranteed benefits and steady protection.

The main difference between the two lies in cost and purpose. Term insurance focuses on pure protection at a lower cost, while whole life insurance combines protection with savings. Life insurance planning should consider your income, financial goals, and family responsibilities. If your goal is maximum coverage at a low cost, term insurance may be the better choice. If you want lifelong coverage and a savings element, whole life insurance may fit your plan.

Budgeting Premiums Effectively

Life insurance planning is most successful when premiums fit comfortably within your budget. Paying premiums regularly is important to keep your policy active and effective. The first step in life insurance planning is to review your monthly income and expenses. This helps you decide how much you can afford without affecting daily needs.

Choose a policy that balances coverage and cost. In life insurance planning, affordable premiums should not mean insufficient coverage. Term life insurance is often preferred by budget-conscious families because it offers high coverage at low premiums. Whole life insurance costs more, so careful planning is needed before choosing it.

Paying premiums annually instead of monthly can sometimes reduce costs. Life insurance planning also involves choosing a payment method that suits your cash flow. Automatic payments can help avoid missed premiums and policy lapses. It is also important to avoid buying unnecessary add-ons that increase costs without clear benefits.

Review your policy as your income grows. Life insurance planning is not a one-time decision. If your salary increases, you may adjust coverage or switch plans. However, never stretch your budget too much, as missed payments can cancel the policy.

Role of Age and Health

Life insurance planning is strongly influenced by age and health. These two factors directly affect premium costs and coverage options. Younger individuals usually pay lower premiums because they are considered lower risk. This makes early life insurance planning more affordable and beneficial. Starting early also allows you to lock in lower rates for a longer time.

Health plays an equally important role. Insurance providers assess health conditions, lifestyle habits, and medical history before offering coverage. In life insurance planning, good health can lead to better policy options and reduced premiums. Smoking, chronic illnesses, and poor fitness may increase costs.

As age increases, premiums generally rise. Life insurance planning for older individuals often requires higher payments for the same coverage. This is why experts recommend starting life insurance planning as soon as financial responsibilities begin. Even small policies started early can provide strong protection later.

Regular medical checkups and healthy habits support better insurance outcomes. Life insurance planning is easier when health risks are managed. Some insurers also offer discounts for healthy lifestyles, making planning more cost-effective.

Conclusion

Life insurance planning is an important step in securing your family’s financial future. By understanding different policy types, assessing family needs, choosing the right coverage, and managing premiums wisely, you can build strong financial protection. Age and health also play a key role, so starting early makes planning easier and more affordable. Life insurance planning is not just about money, but about peace of mind. When done carefully, it ensures your loved ones are protected from financial stress and can maintain their lifestyle even during difficult times. Regular review and smart decisions make life insurance planning truly effective and reliable.

FAQs

What happens if premiums are missed?

If premiums are missed, the policy may lapse after a grace period. This means coverage can stop, and benefits may be lost. Some policies allow reinstatement by paying missed amounts with extra charges. It is important to pay on time or choose automatic payments. Regular payments keep protection active and prevent financial stress for your family later.

Can insurance coverage be increased later?

Yes, coverage can often be increased later, but it may cost more. Age and health changes can affect approval and premium rates. Some policies offer riders that allow extra coverage at certain life stages. Reviewing needs regularly helps decide when increasing coverage is necessary to match growing responsibilities.

Are medical tests always required?

Medical tests are not always required. Some policies offer no-medical or simplified approval options. These are faster but usually have higher premiums or lower coverage limits. Traditional policies with medical exams often provide better rates. The choice depends on health condition, urgency, and coverage needs.

How does inflation affect insurance benefits?

Inflation reduces the real value of future payouts. What seems enough today may not cover expenses later. Some policies offer inflation protection or allow coverage increases over time. Reviewing plans regularly helps ensure benefits stay aligned with rising living costs and future financial needs.